When it comes to mortgages, most people focus on one thing, getting the lowest interest rate. But the lowest rate today doesn’t always lead to the best outcome over time. Interest Rate Averaging is a strategy designed to reduce risk, smooth cashflow, and create flexibility, rather than trying to perfectly time interest rates, which no one can do consistently.

What Is Interest Rate Averaging?

Interest rate averaging means splitting your mortgage into multiple loan portions, each fixed or floating for different terms. Instead of putting your entire loan on one interest rate and one expiry date, you deliberately spread it across short, medium, and long-term rates. The goal isn’t to “win big” on rates. It’s to avoid losing big.

By structuring a loan this way, only a portion of the mortgage is exposed to interest rate changes at any one time, which gives greater control as market conditions shift.

Why This Strategy Works

Interest rates move in cycles. They rise, they fall, and sometimes they do nothing for years. Interest rate averaging helps because:

You’re never fully exposed to sharp rate increases

You still benefit when rates fall

Your loan renewals are staggered, not all at once

You retain flexibility to adapt as your life and finances change

Think of it like investing. You wouldn’t put everything into one asset at one moment in time. Your mortgage deserves the same thinking.

Example: How Interest Rate Averaging Can Look in Practice

Here’s an example of how a $630,000 loan could be structured to balance risk and flexibility.

1. Floating Portion: $30,000

Short-term paydown strategy

Kept on a discounted floating rate

Designed to be paid off aggressively within 12 months

Provides flexibility for extra repayments with no break costs

Once this portion is cleared, another small chunk can be peeled off a fixed loan when it renews and the process repeated. This works especially well when combined with revolving credit or offset accounts, where your income and savings reduce interest daily rather than sitting idle.

2. Short-Term Fixed: $200,000 (1 year)

Aggressive and rate-responsive

Takes advantage of competitive short-term fixed rates

Renews quickly, allowing you to benefit if rates fall

Risk: If rates rise, this portion reprices sooner.

Reward: Keeps part of your loan nimble and responsive.

3. Medium-Term Fixed: $200,000 (2–3 years)

Balance and stability

Still offers sharp pricing

Adds protection compared to a 1-year rate

Helps avoid having all eggs in one basket

This portion forms the backbone of the loan, smoothing out volatility.

4. Long-Term Fixed: $200,000 (5 years)

Security and peace of mind

Slightly higher rate than shorter terms

Locks in certainty for a meaningful portion of the loan

If interest rates rise significantly, this fixed portion acts as an anchor, protecting your household cashflow.

What Happens Under Different Rate Scenarios?

This is where interest rate averaging really shines.

If Interest Rates Rise

Only part of your loan is affected at each renewal

In this example, around two-thirds of the loan is fixed for 2–5 years, so increases happen gradually, not all at once

If Interest Rates Fall

The short-term portion rolls off quickly

You can re-fix at lower rates sooner on part of the loan

If Interest Rates Stay Flat

A large portion of the loan remains at historically reasonable rates

You maintain flexibility without taking unnecessary risk

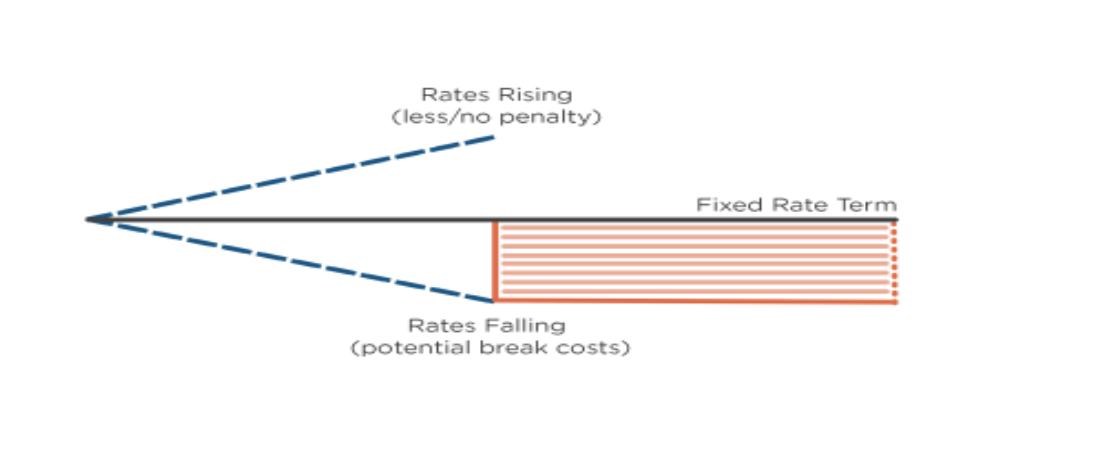

Important Trade-Offs to Understand

Interest rate averaging is about risk management, not absolute minimisation of interest cost.

Some key considerations:

You may not achieve the very lowest possible rate at any one time

Loans don’t all renew together, which can slightly reduce bargaining power

Longer fixed terms can limit extra repayments or incur break costs if plans change

That’s why this strategy works best when aligned with your future plans, such as:

Selling or upgrading a property

Changing banks

Receiving lump sums, including inheritance, bonuses, or business income

Most banks allow limited extra repayments, often around 5 percent, without penalties, which can still be used strategically.

Fix, Float, or Both?

Both fixed and floating rates have strengths and weaknesses.

Fixed rates provide certainty and protection

Floating rates provide flexibility and repayment freedom

Interest rate averaging combines both, allowing you to adjust as interest rates and your life evolve.

The Bottom Line

Interest rate averaging isn’t about predicting the future. It’s about preparing for multiple futures.

By spreading your mortgage across different terms and structures, you create:

Stability when rates rise

Opportunity when rates fall

Flexibility when life changes

And for most homeowners, that balance is worth far more than chasing the lowest rate on paper.

This article is for general information purposes only and does not constitute financial advice. The content is based on information current at the time of writing and may be subject to change. Lifetime Group Limited is a licensed Financial Advice Provider. For advice specific to your situation, please speak with a Financial Adviser. You can view our Disclosure Statement here. All investments involve risk and are not guaranteed. Any examples or projections are for illustration only and should not be relied on as advice.